-1.png)

Building DPDP compliance can cost ₹2.5–18 crore and take up to 24 months. Understand the real cost before you decide.

Compare the best TPRM tools for DPDP compliance in India. See pros, cons, vendor risk features, and why Privy by IDfy stands out.

Learn how cross-border payments work in India, including RBI rules, FEMA compliance, KYC/KYB checks, settlement flows, and fraud risks.

All 6 credit risk types, explained for Indian banks and NBFCs — underwriting, monitoring, and RBI guidelines covered.

A practical breakdown of credit risk modelling in India: PD, LGD, EAD models, Basel III RBI norms, ML approaches, and data requirements.

Understand credit risk assessment models, PD/LGD/EAD, scorecards, and the lending risk process used by Indian banks and NBFCs.

Learn how BNPL works in India, its risks, regulations, business models, and future trends in digital payments and embedded finance.

A practical guide to credit risk management in India — types, RBI framework, 5-step process, tools, and NBFC-specific challenges.

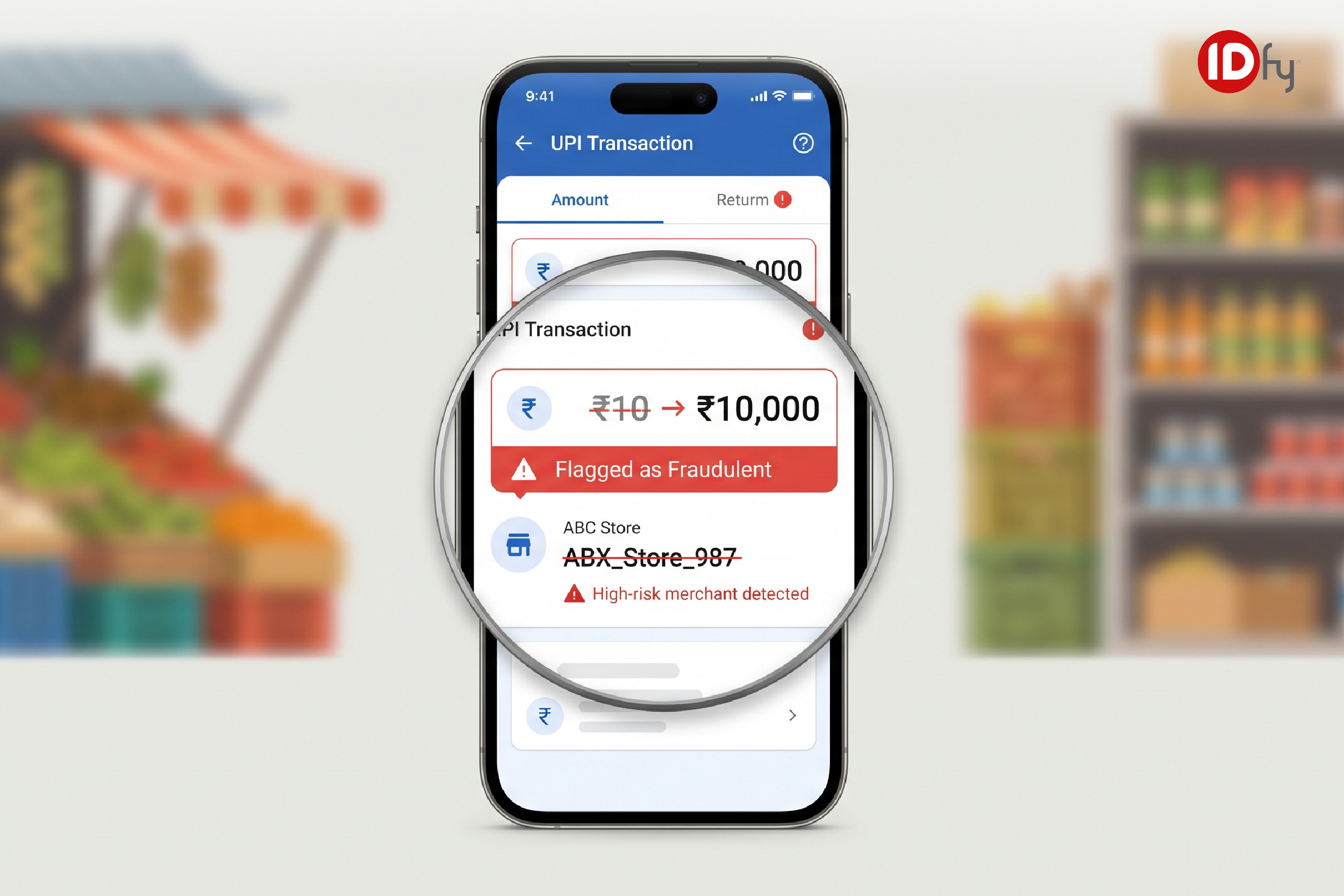

Explore the 2026 payment fraud landscape in India. Learn the most common types of payment fraud, the emerging fraud trends, and how to build a future-ready fraud prevention strategy.

Discover how to optimize driver onboarding through automation and risk assessment. Learn the essential process to ensure safety, compliance, and retention.

Explore IDfy’s breakdown of IRDAI’s 2025 fraud guidelines and learn how insurers can reduce fraud, strengthen compliance, and use real-time intelligence to improve profitability.

Compare the top DPDP compliance software. Discover why Privy by IDfy is the best platform designed for a 90-day implementation.

Kirti Patil

CTO

Abhinav Puneeth

Director

Sameer Jadhav

Vice President

Amarendra Nath Mishra

Group CHRO, Hero Enterprise

Devrat Singh

Senior Product Manager, Blackbuck

Kirti Patil

CTO

Abhinav Puneeth

Director

Sameer Jadhav

Vice President

Amarendra Nath Mishra

Group CHRO, Hero Enterprise

Devrat Singh

Senior Product Manager, Blackbuck

Kirti Patil

CTO

Abhinav Puneeth

Director

Sameer Jadhav

Vice President

Amarendra Nath Mishra

Group CHRO, Hero Enterprise

Devrat Singh

Senior Product Manager, Blackbuck

It’s a complete trust infrastructure. Stop chasing alerts and start preventing fraud from the source with an interconnected platform that sees everything.