On the 10th of May 2021, the Reserve Bank of India (RBI) released its latest amendment to the Master Direction for KYC norms. In it, the RBI incorporated the guidelines for changes that were earlier announced as part of the ‘Rationalization of Compliance towards KYC Norms’.

In this post, we break down these changes for you and show how our existing platform can be leveraged right away to maximize the potential presented by them.

Let’s get straight to it then.

What are the impacted dimensions?

There are three broad categories that have been impacted under the new regulations:

New use cases unlocked for V-CIP

New use cases unlocked for V-CIP- Enhanced security and anti-fraud measures

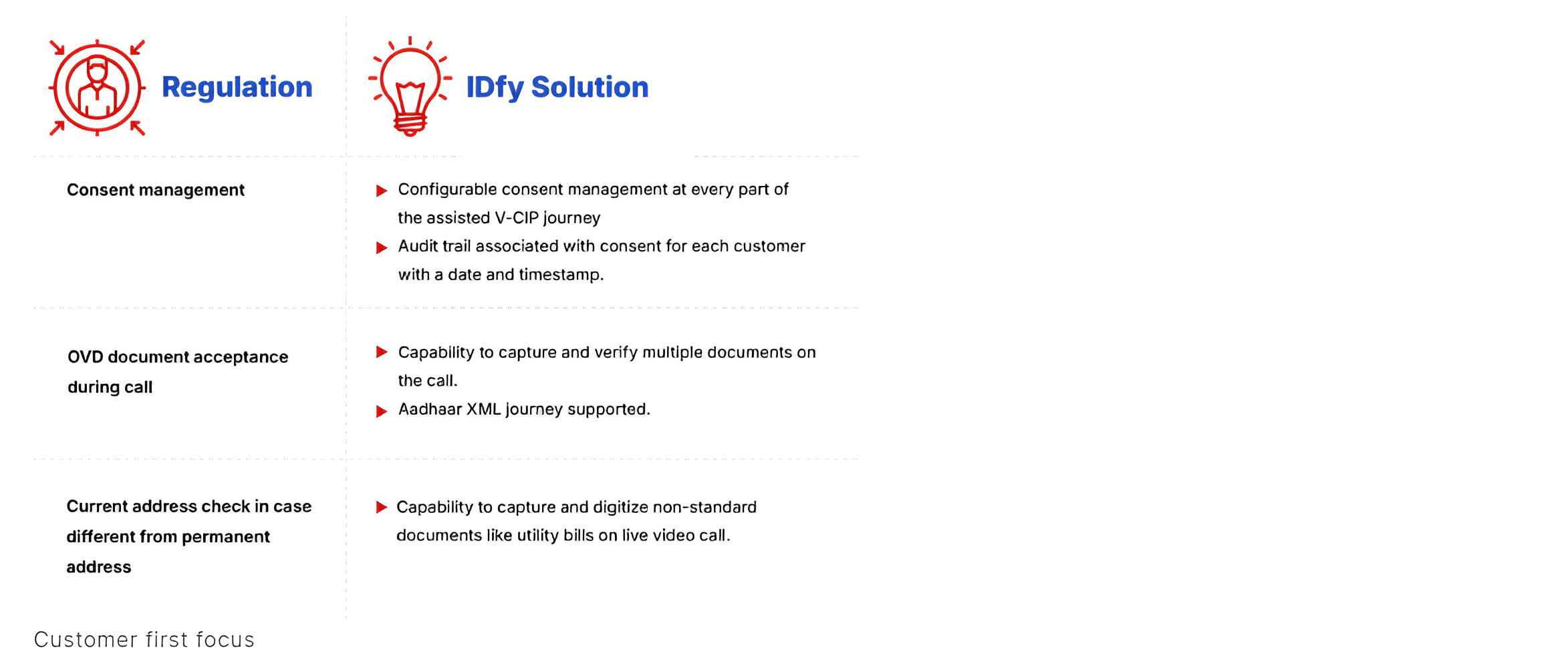

- ‘Customer First’ focus

Let us go through each one in a bit more detail.

New use cases unlocked

New use cases, that were hitherto untouched by V-CIP, have now opened up in a timely manner for digitisation.

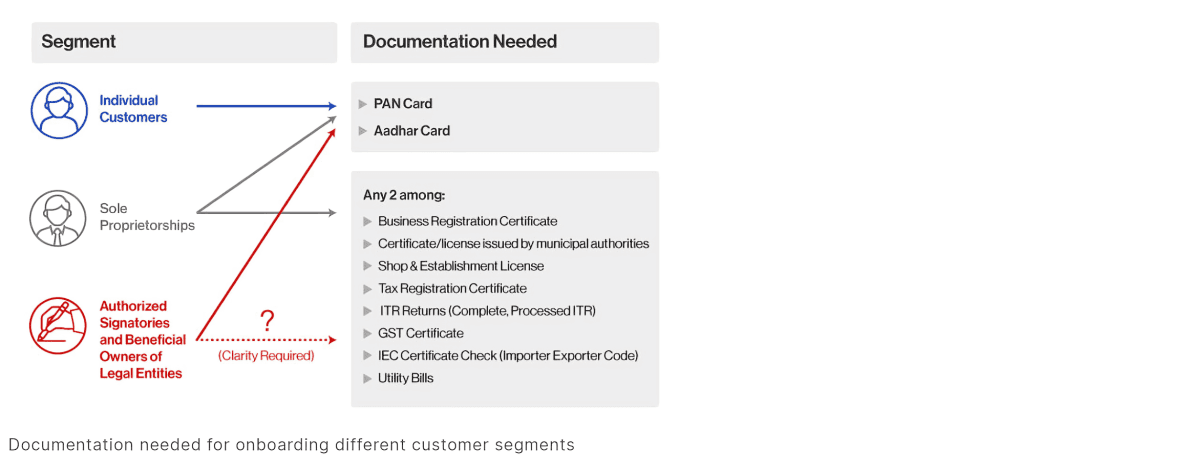

*For onboarding authorized signatories and beneficial owners of Legal Entities, there is still a bit of clarity required in terms of which and how many documents are needed for sufficient verification.

Nonetheless, let’s take a look at the new use cases that have now opened up:

- V-CIP for non-individual onboarding:

- Regulation: V-CIP can be used for onboarding proprietorship firms, authorized signatories and beneficial owners of legal entities.

- Impact: New use cases such as MSME lending, corporate lending and current account opening have opened up for digitisation.

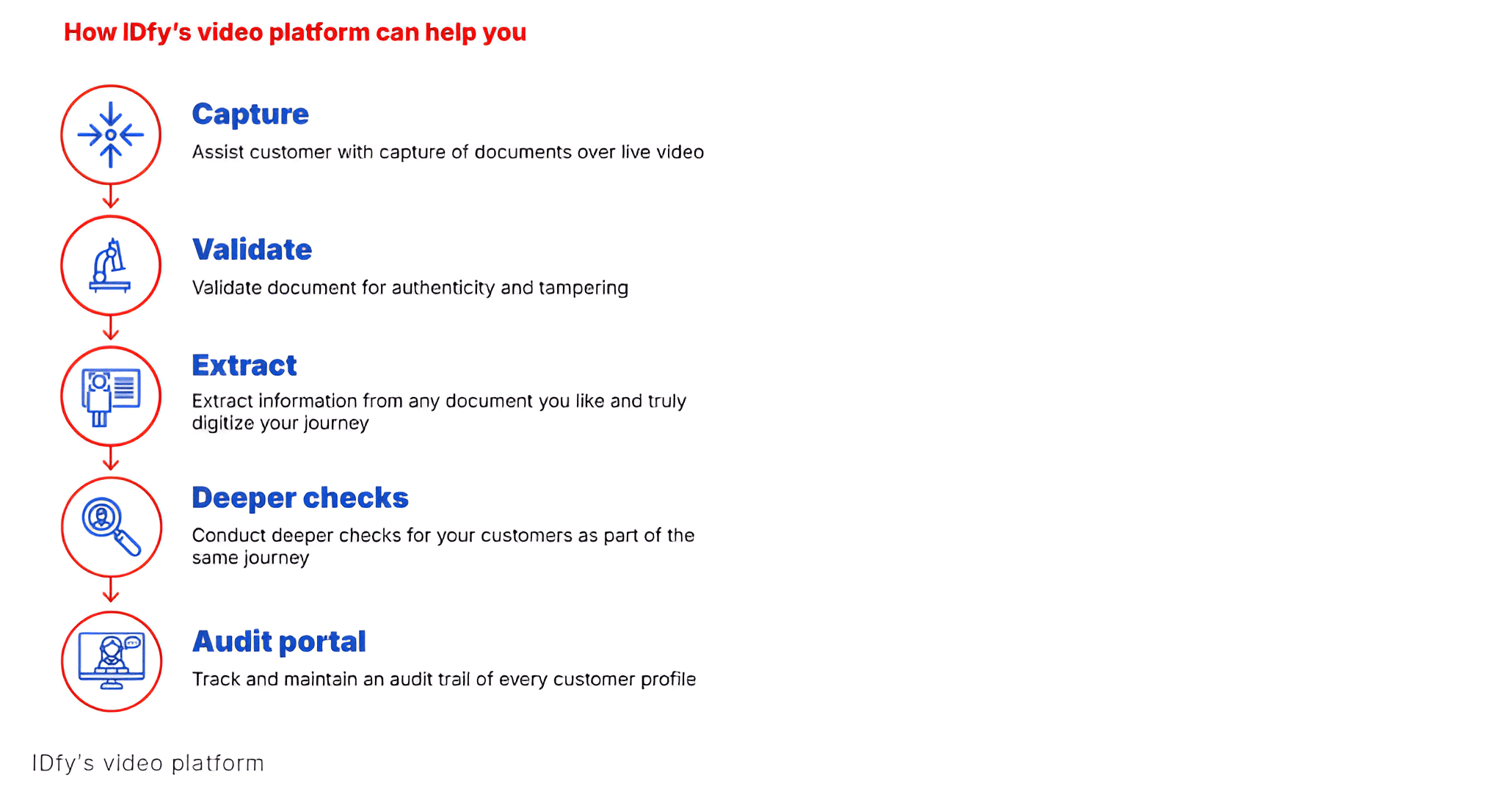

- IDfy solution: Our existing video services platform can be leveraged as it offers the flexibility to capture and verify any required document.

- Conversion of min-KYC accounts to full-KYC accounts:

- Regulation: Accounts opened in non face-to-face mode using Aadhaar eKYC can be converted to full-KYC accounts using V-CIP.

- Impact: Banks can improve on their earlier conversion ratio from min-KYC to full-KYC accounts, save on compliance costs and increase bottom-line revenue.

- IDfy solution: Our existing platform has all the required features to go-live with this use case instantly with full compliance.

- Periodic KYC updation/re-KYC of banking customers:

- Regulation: V-CIP can be undertaken for re-KYC of customers in the following scenarios:

- Change in address

- Minor to major conversion

- Existing KYC documents being of poor quality

- Existing KYC documents have expired

- Change in key personnel for Legal Entity (LE) customer

- Impact: This can significantly improve customer experience and reduce operational expenses spent on chasing dormant customers for KYC updation.

- IDfy solution: Our existing video services platform is well suited for this use case. We can help you examine the quality of existing KYC documents, extract document details and generate capture links for customers eligible for re-KYC.

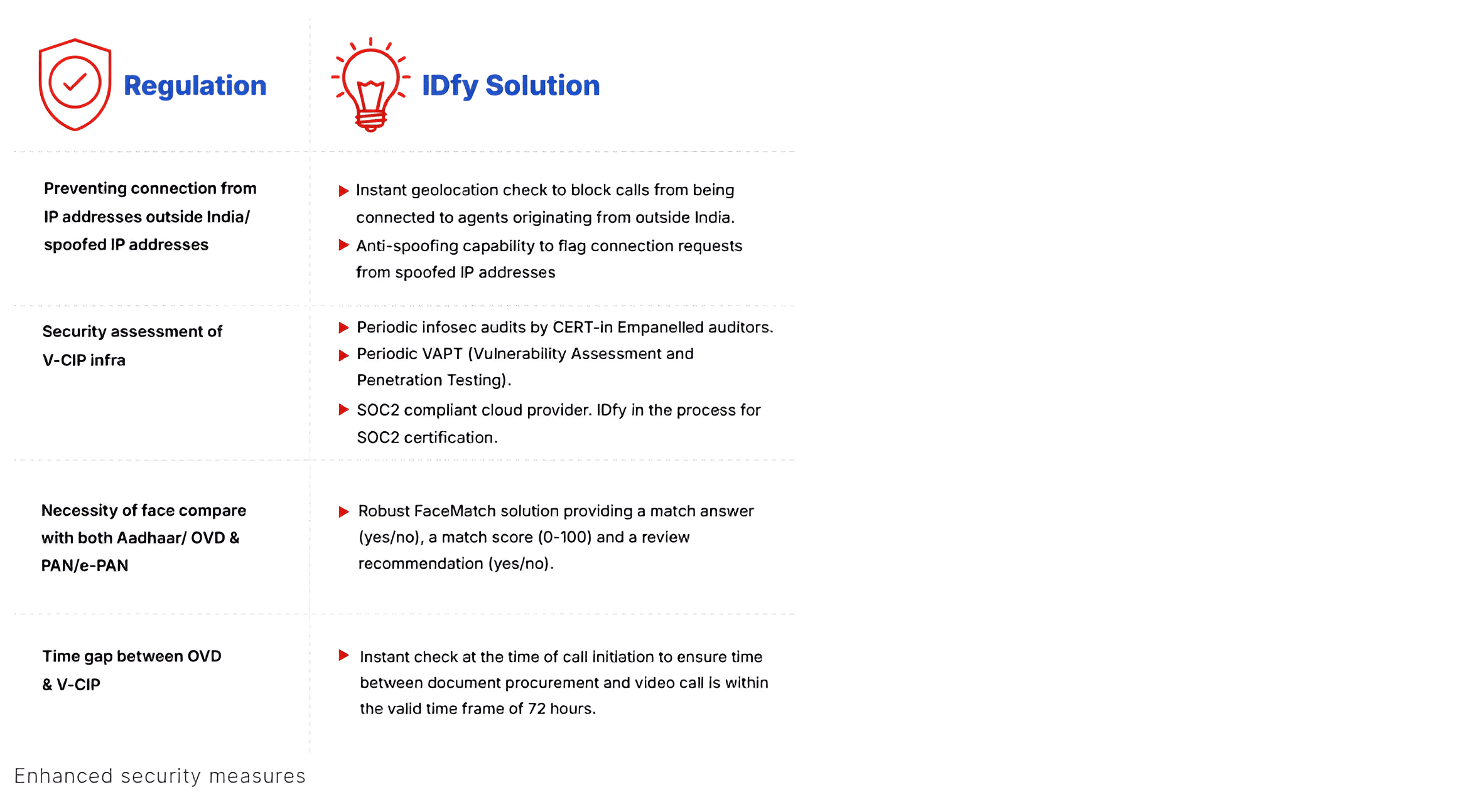

Enhanced security and anti-fraud measures

‘Customer First’ focus

We believe these are changes in the right direction and provide a much needed impetus towards digitisation in the larger banking ecosystem.

Write to us at shivani@idfy.com to know more about how we are helping our clients build new solutions tailored for new and emerging use cases.

IDfy provides identity verification and customer onboarding solutions to some of the leading financial institutions in India.

Follow us on your preferred social media channels for regular updates.