What is KYB?

“Know Your Business” (KYB) is a due diligence process that companies and financial institutions undertake to verify the legitimacy and authenticity of their business partners. Similar to the Know Your Customer (KYC) process, which focuses on individual customers, KYB focuses on businesses. The primary aim of KYB is to establish the authenticity of a business entity, ensuring that it’s a legitimate operation and not a front for illicit activities.

What all are verified during KYB?

The RBI guidelines need FIs to verify the following information about a company during the KYB process:

Legal structure:

FIs must verify the legal structure of the company. That includes its registration documents, articles of association, and memorandum of association. Such information helps banks understand the company’s business structure. It also helps FIs understand the company’s relationship with its owners.

Ownership:

FIs must verify the ownership of the company. That includes verifying the identities of its shareholders and beneficial owners. They must also identify any nominee shareholders. It is also important to understand the nominee shareholders’ relationship with the company.

Management:

FIs must verify the identities of the company’s directors and senior management. They must also understand their roles and responsibilities within the company. Understanding the management team’s relationship with the owners is also important.

Business operations:

FIs must understand the company’s business operations. That includes the company’s products and services, customer base, and suppliers. This information helps assess the company’s risk profile. Understanding the risk profile shows its potential for money laundering or terrorist financing.

Location:

FIs must verify the company’s location and any branches or subsidiaries. They must also understand the company’s relationship with any third-party service providers. Third-party service providers could be accountants or lawyers.

Financial performance:

FIs must collect and verify the company’s financial performance. Financial performance includes financial statements, tax returns, and audit reports. This information helps them assess the company’s financial health. A company with poor financial health has potentially more financial crime risks.

The RBI guidelines need financial institutions to conduct ongoing monitoring of Know Your Business (KYB) checks. FIs must update their KYB information on a regular basis. Whenever there is a change in the company’s ownership, management, or operations, information it should be updated. They must also conduct periodic reviews of their KYB information. This is to ensure that it remains accurate and up-to-date.

FIs must also understand the risks associated with different types of companies. High-risk companies include those in the real estate, jewelry, and precious metals sectors. These industries are susceptible to money laundering and terrorist financing activities. FIs must conduct enhanced due diligence when dealing with high-risk companies. That may include conducting extra verification checks and monitoring their transactions.

Along with the RBI guidelines, banks, and NBFCs must follow other AML and CFT regulations in India. These regulations include the Prevention of Money Laundering Act (PMLA), and the Foreign Contribution Regulation Act (FCRA). They must also follow international AML and CFT standards. Such regulations are set by the Financial Action Task Force (FATF).

FIs must also ensure that their employees are trained to conduct KYB checks. Employees must understand the risks associated with money laundering and terrorist financing activities. They should also understand the legal and regulatory requirements for conducting KYB checks. There must be internal controls in place to ensure employees follow KYB procedures.

The consequences of non-compliance with KYB regulations can be severe for financial institutions. Non-compliance can lead to fines, reputational damage, and even criminal charges. Banks and NBFCs must take KYB compliance seriously. They should invest in the necessary resources to meet regulatory requirements.

Importance of KYB in today’s landscape

Regulatory Compliance: Many jurisdictions around the world now have stringent anti-money laundering (AML) and counter-terrorism financing (CTF) regulations. KYB procedures help businesses stay compliant by ensuring they’re not inadvertently doing business with entities involved in illegal activities. Non-compliance can lead to hefty penalties, legal actions, and significant reputational damage.

Mitigating Financial Crime: By understanding who they are doing business with, companies can avoid associating with entities involved in money laundering, bribery, corruption, or other illicit activities. This is crucial for maintaining the integrity of global financial systems.

Reputation Management: In an age of information, where news spreads quickly, associating with dubious entities can severely tarnish a company’s reputation. Ensuring that business partners are legitimate safeguards a company’s image and credibility in the market.

Building Trust in B2B Relationships: Trust is a cornerstone in business-to-business relationships. By practicing KYB due diligence, businesses convey to their partners that they prioritize transparency, integrity, and legitimate operations. This can enhance mutual trust and pave the way for long-term partnerships.

Operational Efficiency: By having a robust KYB process in place, companies can streamline their partner onboarding processes, making it quicker to establish new partnerships or business relationships.

Risk Management: Beyond financial crimes, understanding a business partner’s operations, financial health, and industry can help in assessing credit risks, supply chain vulnerabilities, and other potential operational risks.

Fostering Ethical Business Practices: By implementing KYB processes, companies can ensure they’re not indirectly supporting industries or businesses that might be involved in unethical practices, such as human rights abuses, environmental degradation, or unfair labour practices.

The Rise of KYB: Historical Context

Brief History of Business Verification Processes

Historically, the concept of “knowing your business” wasn’t as formalized as it is today. In ancient times and even during the early modern era, business was often conducted based on trust built through personal relationships, familial ties, or longstanding trade relations.

Ancient Trade Networks: In ancient times, trade was mainly local, and traders knew their partners personally. When long-distance trade flourished, it was done through established trade networks, with trust being a pivotal factor. There was no formalized KYB, but trust was built over time through repeated interactions.

Guilds and Merchant Associations: In medieval times, guilds and merchant associations often provided a kind of business verification. To become a member, businesses had to meet certain standards and were vetted by peers. Being a member of such a guild was, in itself, a mark of legitimacy.

Introduction of Regulatory Bodies: As the modern economy took shape, the complexities of business relationships grew. Regulatory bodies and trade associations emerged to set guidelines and standards, making it crucial for businesses to “know” their partners, though this was often done through paper-based processes and face-to-face interactions.

Evolution from Traditional Methods to Digital KYB Solutions

With the advent of technology and the increasing complexity of the global business landscape, the need for a more streamlined, efficient, and reliable way to verify businesses became apparent.

Early Computerization: As computers started making their way into businesses in the 20th century, data about businesses began to be digitized. Companies would maintain databases of their suppliers, partners, and customers. However, these were still largely isolated databases and not part of a comprehensive verification process.

Globalization and Internet Era: The globalization of business meant that companies now had partners across the world. The internet provided a platform where information about businesses became accessible, leading to the creation of online business directories and databases. However, while access to information increased, so did the chances of fraud and misrepresentation.

Regulatory Push: The late 20th and early 21st centuries saw a significant push in regulations around financial transactions, especially post events like the 2008 financial crisis. Anti-money laundering (AML) and counter-terrorist financing (CTF) rules became stricter, necessitating a robust KYB process.

Rise of Digital KYB Solutions: With advancements in technology and the need for robust KYB processes, specialized digital KYB solutions emerged. These platforms used a combination of:

Big Data Analytics: To sift through vast amounts of data quickly and identify patterns.

AI and Machine Learning: To automate the verification process and continuously learn and improve.

Blockchain Technology: To maintain immutable records of business verifications.

API Integrations: Allowing for real-time checks with various databases and registries globally.

Benefits of Digital KYB: Digital KYB solutions provide unprecedented efficiency, speed, and accuracy. They reduced the need for manual checks, reduced errors, and ensured that businesses remained compliant with evolving regulations. Moreover, they allowed for continuous monitoring, ensuring that the KYB process wasn’t just a one-time check but an ongoing part of the business relationship.

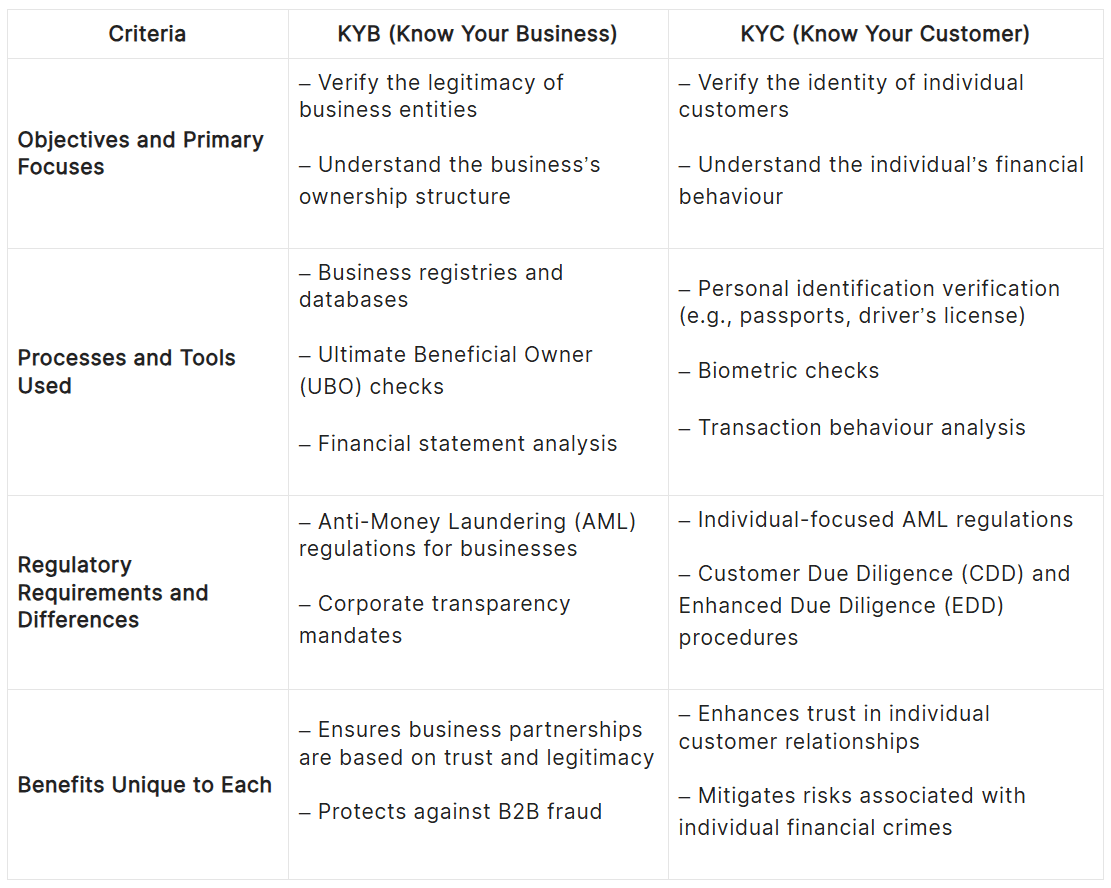

Differences between KYB (Know Your Business) and KYC (Know Your Customer)

Why is KYB Important?

- Mitigating Fraud and Financial Crimes

Nature of Crimes: In our increasingly globalized and digital world, the instances of financial crimes, such as money laundering, bribery, fraud, and embezzlement, have grown both in complexity and scale. Criminal enterprises often use business entities as fronts or intermediaries to hide or move illicit funds, disguise ownership, or otherwise obscure illicit activities.

Nature of Crimes: In our increasingly globalized and digital world, the instances of financial crimes, such as money laundering, bribery, fraud, and embezzlement, have grown both in complexity and scale. Criminal enterprises often use business entities as fronts or intermediaries to hide or move illicit funds, disguise ownership, or otherwise obscure illicit activities.- Role of KYB: Through the Know Your Business (KYB) process, companies can thoroughly vet and verify the authenticity and legitimacy of their business partners. This ensures that they are not inadvertently facilitating or becoming involved in illicit activities, shielding themselves from both the moral and legal repercussions of such engagements.

- Regulatory Compliance and the Role of Governments

- Stringent Regulations: Over the past few decades, governments around the world have introduced strict regulations to prevent money laundering, terrorist financing, tax evasion, and other financial crimes. Regulations often mandate businesses, especially financial institutions, to perform due diligence on their partners.

- Government Oversight: Governments, through various regulatory bodies, ensure that businesses adhere to these regulations. Non-compliance can result in significant penalties, sanctions, legal actions, and loss of operating licenses.

- Role of KYB: KYB processes help businesses to stay compliant with these regulations. By systematically verifying and monitoring business partners, companies can demonstrate to regulatory bodies that they have taken the necessary steps to ensure they’re only doing business with legitimate entities.

- Protecting Business Interests and Reputation

- Brand Image and Reputation: In the age of information, a company’s reputation is one of its most valuable assets. Associations with dubious or illicit entities can severely tarnish a company’s image, potentially leading to lost business opportunities, decreased customer trust, and reduced shareholder value.

- Operational Risks: Beyond reputation, there are operational risks involved in partnering with unverified entities. There could be financial losses due to fraud, disruptions in supply chains, or legal complications.

- Role of KYB: By ensuring that all business partners are thoroughly vetted and verified, companies can safeguard their reputations and mitigate potential operational risks. This proactive approach demonstrates a company’s commitment to ethical and transparent operations.

- Building Trust in B2B (Business-to-Business) Relationships

- Trust as a Foundation: In B2B relationships, trust plays a fundamental role. Businesses need assurance that their partners will honour contracts, deliver on promises, and act in good faith. Likewise, businesses want to be certain that their partners’ operations are transparent and legitimate.

- Long-term Partnerships: Trustworthy relationships often lead to long-term partnerships, which can offer both companies stability, consistent business growth, and collaborative opportunities.

- Role of KYB: The KYB process is a concrete step towards building this trust. By transparently sharing information and willingly undergoing verification, businesses signal to their partners that they have nothing to hide. Similarly, by performing KYB checks, companies show that they value integrity and transparency, setting a positive foundation for the B2B relationship.

What is a KYB solution?

A KYB solution is a technology-enabled business process management solution. It lets financial institutions run a comprehensive KYB check on businesses. The critical components of a KYB solution comprise:

- Collecting Personal Identifiable Information (PII)

- Gathering supporting documentation

- Verifying the available information & documents

IDfy has a best-in-class Know Your Business (KYB) solution in place which has been used by our customers to onboard thousands of merchants. You can learn all about it here: Click Now.

In conclusion, KYB verification is a critical component for financial institutions to follow AML and CFT requirements. It also plays a crucial part in managing risk and preventing ID and business fraud.