Strangely, there was nothing subtle about the group’s modus operandi. As per media reports Between 2009 and 2013, they have cheated a consortium of 10 banks, siphoning the money off through bogus invoices, round-tripping, and related-party transactions.

This wasn’t a one-off heist either. Between 2009 and 2013, their company repeatedly borrowed significant sums of money without giving a whiff to their lenders of the massive theft that was underway. Only when the NPA hit the fan did they realize that they were funding the lavish life of a business tycoon.

Underwriting Hindsight is 20/20

Practitioners would claim that a bank’s lending decision is more art than science. But the looming question is – could this have been prevented?

The short answer is – yes. Banks consider a host of quantitative and qualitative data points while making lending decisions. But did you know that the legal history of an individual could impact their creditworthiness?

Credit history and bureau checks provide data about the ability and repayment behavior of borrowers. But how do you know about their “willingness” to repay your loans? This gets even trickier with NTC (new-to-credit) customers. Legal history can act as a great proxy in determining the intent of your borrowers.

Statistically, 84% of companies and 32% of individuals with a past criminal offense indulge in crime again (Based on a correlation study conducted by CrimeCheck on court records, available here). However, the type of offense they are involved in plays a key role in ascertaining their financial standing. For instance, an individual involved in an income tax violation case poses a much higher financial risk than somebody involved in a car accident case.

Nevertheless, no lender would bear the risk of financing a repeat offender, provided this information is available for the lender during underwriting.

Search the Dirt

If you’re a lender, you might wonder how much of this information is truly accessible to you? Would you get detailed information on all pending legal cases against your applicant? Is this information accurate? How reliable is it?

Well, there’s something called a “CrimeCheck Report” that does just that.

It is possible to scrounge through data across various institutions – from all levels of judiciary and tribunals to FIRs – and extract any relevant information about the individual in question.

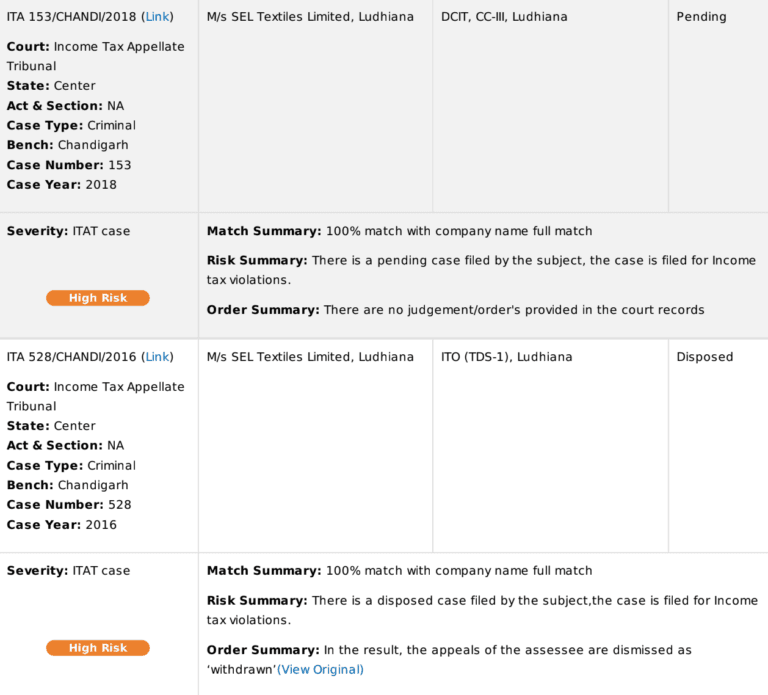

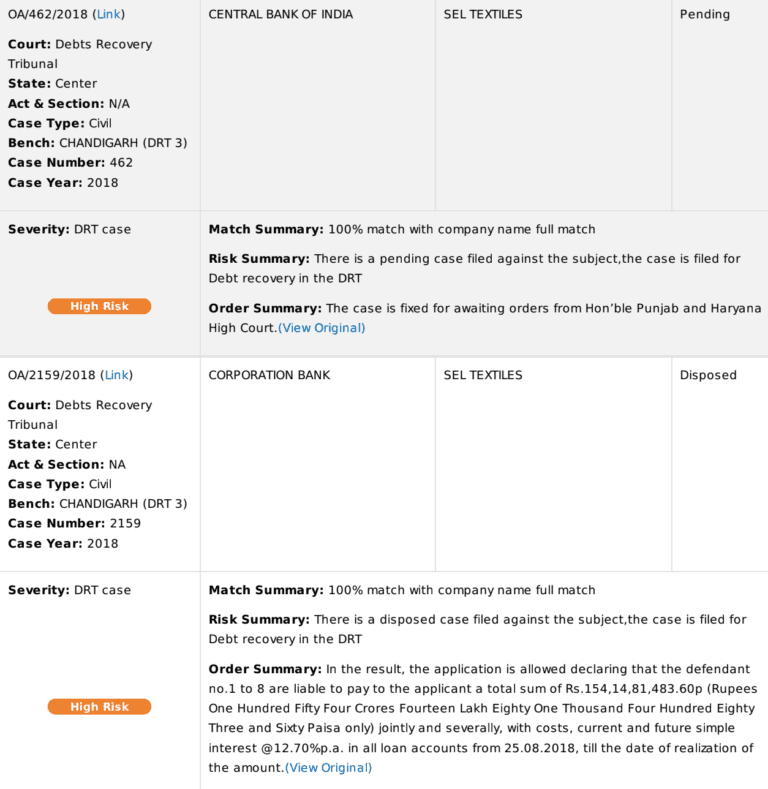

If SEL’s lenders had access to such a report, they would have known that SEL Textiles had 60 registered cases. Between 2015 to 2018, SEL was involved in multiple income tax violation cases in the ITAT (Income Tax Appellate Tribunal).

ITAT matters are generally very detrimental because of the massive fines the Income Tax Department slaps if a company is found guilty. Fines to the tune that is enough to put many businesses out of operation.

During the same period, multiple cases were filed against SEL for debt recovery in the DRT (Debt Recovery Tribunal) – suggesting they were already defaulting on their payment obligations.

The report would go on to provide the breakdown of other such SEL Textile cases by various institutions and give lenders the information that 90% of those open cases were classified as high-risk, implying a high impact on the financial liability of the individual. Had this information been available to lenders during the due diligence process, they most likely would have decided not to lend to SEL.

Due Diligence Swiss Knife

There is no dearth of tools to dig deeper. For instance, a simple analysis of SEL Textiles’ GST would have revealed a conflict in payments to vendors that were related parties. Transactions involving abnormally high amounts of money could have been highlighted and scrutinized further to reveal the nefarious round-tripping that was prevalent at SEL.

Peeling the Swiss Knife further would have brought out the Peer Comparison report, which would have compared transactions made by SEL Textile with those of a comparable firm and thrown up anomalies. This would have alerted the lenders about suspicious transactions.

Cross-referencing filings under the ITR with other documents, such as bank statements or other MCA filings would have revealed any discrepancies, providing crucial data points for the lender to make an informed decision.

As it turns out IDfy has all these checks in its suite of APIs that reduce risks for lenders. If you’re curious to know more, you can get in touch with me.

India and Singapore launching payments via UPI

With the upcoming launch by PM Modi, UPI users can instantly transfer funds with ease from an Indian bank across the border to Singapore while saving fifty percent of transaction fees. Moreover, Malaysia’s merchant trade Asia in collaboration with NIPL allowed sending remittances through UPI in 2021.

You can read more about it here.

UPI volume cap to be altered: NCPI and RBI

NPCI and RBI are in discussion of limiting the volume cap for third-party applications to thirty per cent. This will help control the concentrated risk that may arise if the market cap remains as it currently is. NPCI has been examining all the possibilities and is likely to decide on the issue of UPI market cap implementation by month-end.

You can read more about it here.

Web3 can transform financial data collection: FM Nirmala Sitharaman

With rising technology usage and its adaptation, Web3 is a game changer. Union FM Nirmala Sitharaman touched upon the benefits of Web3 in smoothening the process to restore, operate and report financial data while addressing the 21st World Congress of Accountants.

You can read more about it here.

On a lighter note…

.jpg)